Polish and Czech hotels on the radar

Hotels

This year’s European Investor Intentions Survey was answered by 336 real estate investors, all of whom have a significant interest in the hospitality industry. “We hope to provide a clearer picture of the future shape of the regional hotel investment market. The results reflect the intentions of the investors surveyed, and take into account both current and future geopolitical events that include, but are not limited to, the UK’s withdrawal from the European Union, the Irish and Italian elections and the Catalan independence movement,” writes CBRE.

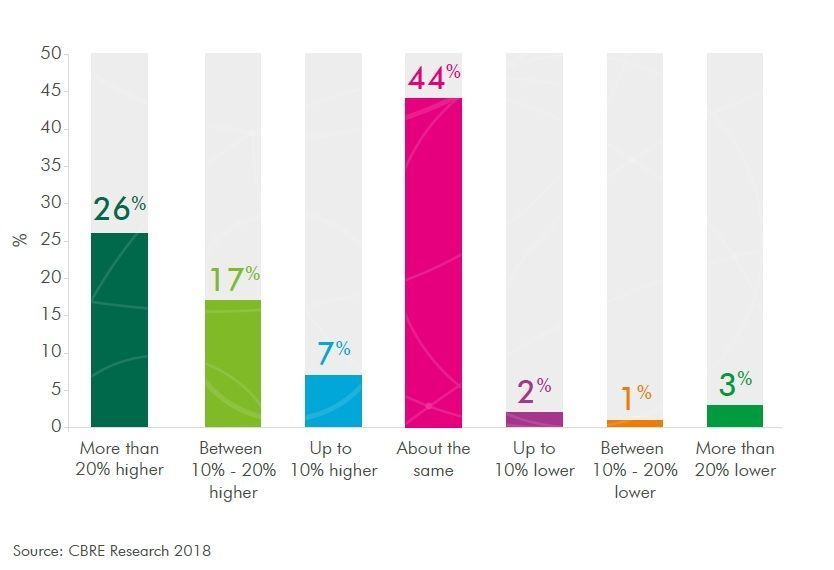

CBRE found that an overwhelming majority of investors surveyed intend to invest either the same amount or more in hotel real estate over 2018, as they did in 2017. The biggest mover in percentage terms is the proportion of investors seeking to invest between 10 pct and 20 pct more capital in 2018. This has risen from 10 pct to 17 pct this year, which is an indication of growing satisfaction with investment performance.

These statistics show a growing attractiveness of hotels relative to other real estate asset classes at a time when markets are becoming increasingly unpredictable. Such findings are underscored by transactional evidence, such as the sales of several major hotel portfolios and operating platforms across the region in 2017.

According to the survey results, the most attractive countries for hotel investment are the UK, Germany and Spain. In ninth and tenth place are Poland (rising one place since last year) and the Czech Republic (which came twelfth in 2016). Eastern European markets are being increasingly targeted by the more opportunistic funds because of strong growth in recent times. North American private equity funds will continue to look for opportunities in these markets in order to meet their typically higher rates of return requirements. “2017 was a record year both in terms of volume and the number of hotel transactions in Poland. Around EUR 350 mln was invested into Poland’s hotel sector last year – a growing investor appetite that we expect to continue throughout 2018,” said Marta Abratowska-Janiec, a senior consultant in advisory services, Poland.

Investment capital is coming from Europe (65 pct), Asia Pacific (15 pct), the Americas (13 pct) and Middle East and Africa (7 pct).

The most notable year-on-year change is the surge in prominence of European capital within the market. European funds represent by far the biggest percentage (65 pct) of the whole sample. This is 23 percentage points up on the findings in CBRE’s 2017 survey. Europe’s importance has grown at the expense of all three of the other regions, with Asia Pacific down from 18 pct to 15 pct, the Americas falling from 18 pct to 13 pct and the Middle East and Africa dropping from 11 pct to 7 pct. This is largely due to widespread European economic growth.

CBRE expects capital from Hong Kong, Singapore and other Southeast Asian countries to increasingly dominate flows from Asia Pacific, following a slowdown in Chinese investment due to the imposition

of outbound capital restrictions. From the Americas, North American private equity funds are expected to be increasingly active in Southern and Eastern Europe, due to the potential for higher rates of return. Among Middle Eastern and African investors, much of the capital will continue to emanate from the Gulf Cooperation Council (GCC) nations despite the relatively low price of oil.

“A low-yield environment and shortage of good-quality investable stock continues to present a challenge to property investors seeking opportunities to deploy capital. Throughout this cycle, we have seen a growing number of institutional investors become active in hotel space, amid increasing transparency and a growing understanding of the sector. The majority, if not all, have gone on to benefit from relatively high risk-adjusted returns, in addition to the enhanced diversification benefits that hotels can deliver to their portfolios,” explains Joe Stather, the associate director in the investment advisory, EMEA, at CBRE.

Investor appetite could remain unsated due to a shortage of investible stock in 2018. Of the investors surveyed, only 30 pct said they would consider divesting

their hotel assets in the coming year. CBRE saw something similar in the 2017 survey and it would be safe to conclude that this ongoing imbalance between supply and demand may well drive further inflation In hotel asset prices across Europe. There are few surprises in the potential sources of future hotel stock, with the typically active and opportunistic private equity firms and private property companies saying they would be most likely to consider asset sales.

Only 7 pct of respondents claimed they would be investing more than EUR 500 mln, reflecting the limited number of players with the scale to invest at that level. However, some private equity firms stated that they are considering investing as much as EUR 500 mln to EUR 1 bln in the year ahead, which suggests a continued demand for the wider portfolio and platform acquisitions that were a feature of 2017.

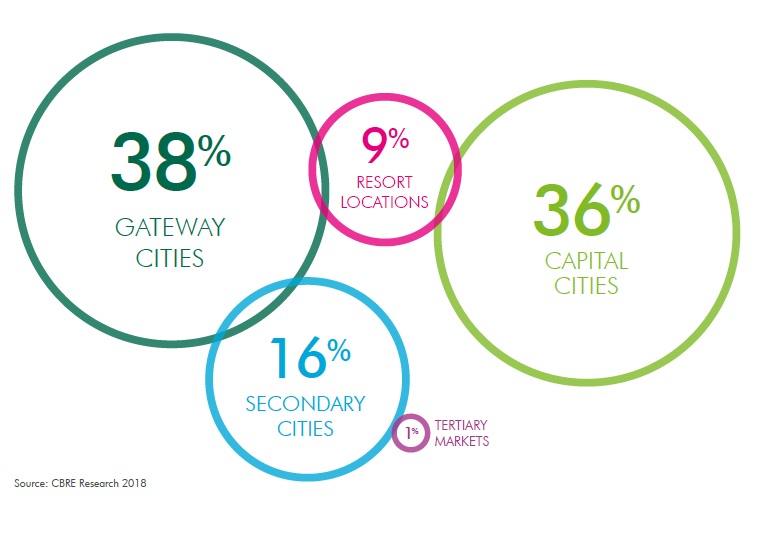

In Europe, what location type for investment purchases in 2018

An open door to redefining the commercial real estate market in Poland

An open door to redefining the commercial real estate market in Poland

Walter Herz

The investment slowdown in the commercial real estate sector that we have been observing in Poland for over a year is primarily the result of the tightening of monetary policy arou ...

The retail sector is not slowing down

The retail sector is not slowing down

Walter Herz

The pandemic, conflict in Ukraine as well as inflation and high interest rates that recent years have brought have reshaped the real estate market around the world. The global slow ...

Retail parks – current opportunities

Retail parks – current opportunities

Avison Young

Over the last few years, retail parks in Poland were mostly developed in smaller formats, around 5,000 sqm, either adding to the existing retail landscape or introducing modern ret ...