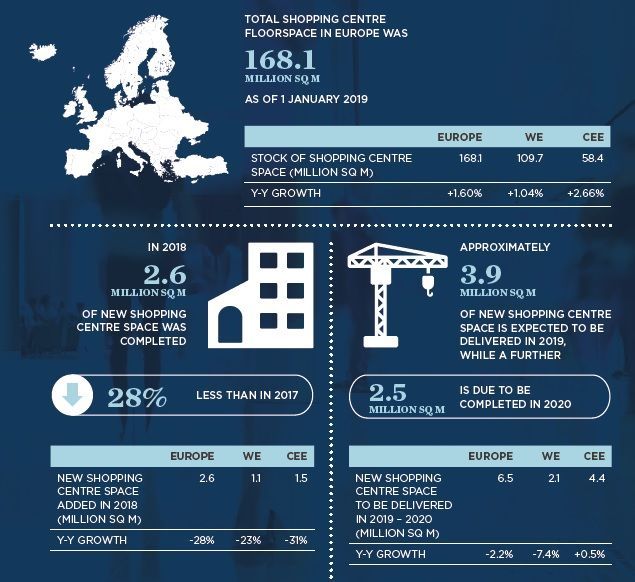

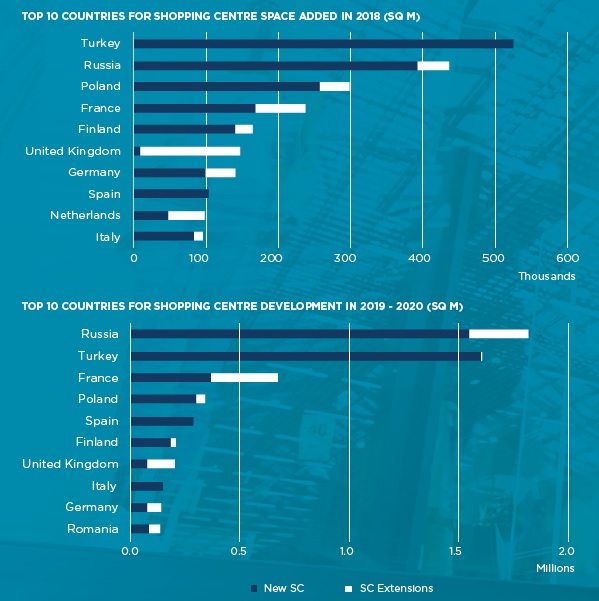

Russia and Poland: half of openings in Europe

Retail & leisure

Shopping centre development slowed down in Western Europe, where annual completions declined by 23 pct. France retains its top position for shopping centre development in this region, despite a 28 pct decrease, when compared with the amount of space opened in 2017. While a similar trend was also seen in a number of other Western European countries, slightly improved results were recorded in Germany, Finland or Sweden.

Central and Eastern Europe also recorded a strong (31 pct) decline in shopping centre development in 2018. While development has decreased across the whole region, Turkey experienced the strongest drop in completions, from 1 mln sqm in 2017 to 0.5 mln sqm in 2018. However, Turkey, Russia and Poland were the most active countries and together they accounted for nearly 50 pct of new openings in Europe.

Development is expected to remain stable over the next two years, with 6.5 mln sqm currently in the pipeline and due to be delivered over 2019-2020. In the majority of European countries, the shopping centre market is approaching maturity and demand for shopping centre space is in relative equilibrium with supply. While the pace of new development has een slowing over the last five years, the total size of the market is still increasing and shopping centre competition is strengthening.

Developers are trying to retain their market positions and are focused on redevelopment and refurbishment projects aimed at creating sophisticated, modern and more aesthetically pleasing shopping and leisure places. Opportunities for new development are seen mainly in two types of schemes. First - dominant innovative schemes with a strong leisure component, which can replace aging and unappealing schemes or secod - smaller convenience/community retail schemes, where a distance to the store, presence of food operator and well curated tenant mix are crucial factors in a scheme’s success. However, it is expected that this will lead to an even stronger polarization in the shopping centre market, with competitive prime schemes on the one hand and struggling secondary schemes on the other hand. Consequently, this is expected to result in the re-purposing of existing secondary retail space to office, residential and other uses. In essence, many shopping centres are likely to be transformed into mixed-use schemes.

Shopping centre developers are also expected to experiment with other existing or new retail formats. Landlords will continue to test different sizing and tenant mixes, while leasing risk is also being shifted from occupiers to landlords as more and more flexibility is required.

An open door to redefining the commercial real estate market in Poland

An open door to redefining the commercial real estate market in Poland

Walter Herz

The investment slowdown in the commercial real estate sector that we have been observing in Poland for over a year is primarily the result of the tightening of monetary policy arou ...

The retail sector is not slowing down

The retail sector is not slowing down

Walter Herz

The pandemic, conflict in Ukraine as well as inflation and high interest rates that recent years have brought have reshaped the real estate market around the world. The global slow ...

Retail parks – current opportunities

Retail parks – current opportunities

Avison Young

Over the last few years, retail parks in Poland were mostly developed in smaller formats, around 5,000 sqm, either adding to the existing retail landscape or introducing modern ret ...